The Vanguard Growth ETF Portfolio (VGRO) has been a staple of many do-it-yourself investor portfolios since its launch in January 2018—becoming, along with its siblings VBAL and VCNS, the first asset-allocation exchange-traded funds (ETFs) in Canada.

For a 0.24% management expense ratio (MER), you get an all-in-one mix of 80% global stocks and 20% bonds, rebalanced periodically, with a Canadian home bias to improve tax efficiency and reduce currency risk. Despite its growth bias, it pays a not inconsiderable quarterly dividend. If imitation is a form of flattery, VGRO comes highly praised: there are now copycats out there from other providers—XGRO, ZGRO, TGRO, HGRW—all with lower MERs.

VGRO holdings

What stocks does VGRO have?

Vanguard U.S. Total Market Index ETF 35.14% Vanguard FTSE Canada All Cap Index ETF 24.65% Vanguard FTSE Developed All Cap ex North America Index ETF 14.44% Vanguard Canadian Aggregate Bond Index ETF 11.83% Vanguard FTSE Emerging Markets All Cap Index ETF 5.47% Vanguard Global ex-U.S. Aggregate Bond Index ETF (CAD-hedged) 4.23% Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged) 4.21%As of April 30, 2025

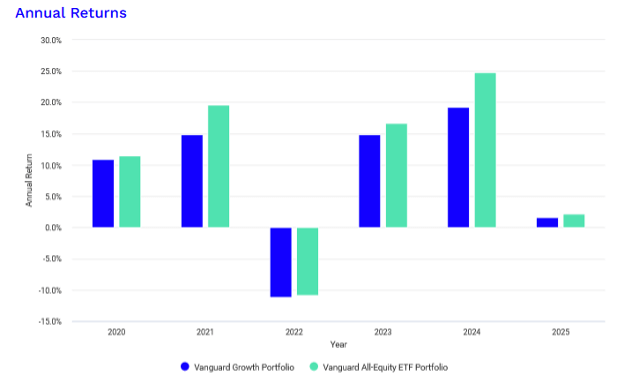

The VGRO ETF and its peers aren’t perfect, nor are they as “safe” as some Canadian investors might assume. In fact, during 2022, VGRO’s price fell 11.19%, a deeper drawdown than its 100% stock counterpart, the Vanguard All-Equity ETF Portfolio (VEQT).

Source: Portfolio Visualizer

Source: Portfolio Visualizer

That’s because VGRO’s 20% bond sleeve, typically a buffer against stock losses due to its usual negative correlation, also dropped sharply in the face of rising interest rates. The average duration of VGRO’s bond holdings is 6.8 years, which means it’s fairly sensitive to rate hikes. All else being equal, a 1% rise in rates could lead to roughly a 6.8% price decline in the bond component alone. And in 2022, this occurred during an equity bear market, exacerbating losses for VGRO.

If you’re concerned about a repeat of this scenario—where both stocks and bonds fall together—there are ways to shore up VGRO’s weaknesses, or that of any stock-and-bond-based portfolio. Here are two TSX-listed ETF ideas worth considering, along with the trade-offs and what you’ll want to watch out for.

The best ETFs in Canada

Holding cash along with VGRO

With the Bank of Canada holding rates steady at 2.75%, investors still have the option to keep some cash reserves in their portfolio earning a decent yield without taking on meaningful risk. Cash is a viable asset class. It doesn’t have the equity risk of stocks, and it avoids the credit or interest rate risk you get with bonds. When both stocks and bonds fall at the same time, cash is one of the few things that still holds its value.

In those moments, cash is king and far from being a dead weight. In fact, Warren Buffett (or rather his successor, Greg Abel) holds nearly $350 billion worth in Berkshire Hathaway. That said, there’s a smarter move than simply leaving money sitting in your brokerage account.

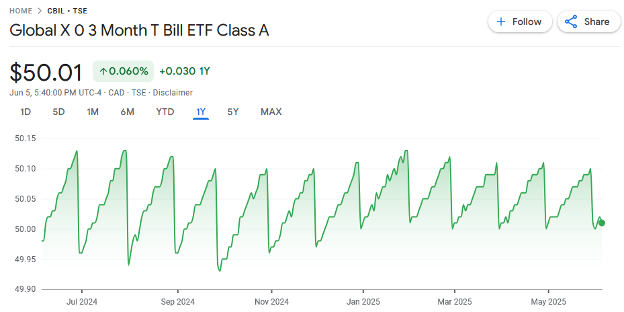

I prefer something like the Global X 0–3 Month T-Bill ETF (CBIL). This ETF invests in ultra short-term federal government-issued treasury bills and essentially returns the Bank of Canada’s policy rate minus its fees. With a 0.11% management expense ratio, the ETF currently yields about 2.58% annualized.

It’s also highly liquid, with a one-cent bid-ask spread and minimal price fluctuation. The way it works is simple: its price ticks up slowly throughout the month, then drops slightly on the ex-dividend date by the amount of income earned that month—like a sawtooth pattern.

Source: Google Finance, CBIL price return chart.

Source: Google Finance, CBIL price return chart.

You’re not going to make a fortune with CBIL, but you won’t lose money either. A 10% allocation to CBIL alongside VGRO could provide a useful buffer. Scale up or down depending on your risk tolerance.

That being said, the main benefit of CBIL is largely psychological: when the markets get ugly, it’s comforting to have one part of your portfolio still green. It gives you breathing room and helps keep the panic in check. Don’t expect this ETF to do much on its own over the long-term.

Include an alternative asset when buying VGRO

The second way to diversify VGRO is by adding an asset that it doesn’t hold at all: gold. This asset has long been considered a structural diversifier in portfolios for a few reasons.

Gold doesn’t rely on earnings or interest payments like stocks and bonds do. Instead, its value is driven by factors like central bank buying, geopolitical uncertainty, inflation concerns, and its status as a finite resource.

Mathematically, gold also plays well in a portfolio setting. Its current monthly correlation to the global stocks and bonds in VGRO is just 0.09, meaning it tends to move independently from those assets.

VGRO versus GOLD monthly correlation

| VGRO:CA | Vanguard Growth Portfolio | 1.00 | 0.09 |

| *GOLD | Gold Price Index | 0.09 | 1.00 |

This low correlation is key. It implies that when other parts of your portfolio are struggling, gold has a higher chance of holding steady or even rising. And because gold is fairly volatile in its own right, you don’t need a huge position for it to make an impact.

For example, a 90/10 mix of VGRO and gold from January 2019 to May 2025 would have produced better risk-adjusted returns.

VGRO versus VGRO + 10% gold

| Start balance | $10,000 | $10,000 |

| End balance | $18,524 | $19,231 |

| Annualized return (CAGR) | 10.08% | 10.73% |

| Standard deviation | 11.21% | 10.24% |

| Best year | 19.30% | 19.92% |

| Worst year | -11.19% | -10.02% |

| Maximum drawdown | -16.08% | -15.21% |

| Sharpe ratio | 0.71 | 0.83 |

| Sortino ratio | 1.10 | 1.30 |

If you’re looking to hold gold in your portfolio, I personally like the BMO Gold Bullion ETF (ZGLD). It’s backed by one of Canada’s largest ETF issuers, physically holds gold in vaults, and has over $1 billion in assets under management. The 0.23% MER is fair given the structure.

Buyer beware: Gold is not a productive asset. It doesn’t generate income like interest or dividends, so it works best as a counterweight to other holdings. To benefit from its diversification properties, you’ll need to rebalance regularly, either annually or quarterly, to maintain your target allocation.

Should you add other ETFs to VGRO?

A few years ago, my answer might’ve been no. The Canadian ETF market didn’t offer much beyond the basics, and anything outside plain stock or bond exposure (alternatives) was usually expensive and illiquid. That’s changed. And options like CBIL and ZGLD are as cheap as it gets here.

Today’s investable universe goes well beyond stocks and bonds, and in a world where the macro backdrop has shifted after many decades of steadily falling interest rates to higher-for-longer, diversification matters.

U.S. versus Canada long-term interest rate trend

Source: YCharts

It’s simply about diversifying your diversifiers. When stocks stumble, bonds usually help. When bonds fail, gold can step in. And if everything drops at once, cash acts as your dry powder.

The key is discipline. If you’re going to add ETFs to your portfolio, use the lowest-cost, most liquid options and commit to managing your asset allocation. That means setting target weights and rebalancing regularly, no matter how markets behave.

If, after all that, your plan is still just “VGRO and chill,” that’s perfectly fine, too. Over the long term, consistency beats complexity every time.

Get free MoneySense financial tips, news & advice in your inbox.

Read more about ETF investing:

How to invest in Canadian bank ETFs Best online brokers in Canada Reducing risk in an RESP: How to invest as your kid approaches college How to invest tax-free in a bitcoin ETF in CanadaThe post Is VGRO a good investment? What else should I buy? appeared first on MoneySense.

Bengali (Bangladesh) ·

Bengali (Bangladesh) ·  English (United States) ·

English (United States) ·