Evan Knopp, Commercial Strategy and Marketing at Medscout

Evan Knopp, Commercial Strategy and Marketing at Medscout

A Shoulder Replacement Case Study

The Bottom Line: When CMS makes a procedure ASC-payable, the shift is fast, measurable, and concentrated in certain territories. Here’s what total shoulder arthroplasty can tell us about where the site-of-service mix for hundreds of procedures is headed.

In July, I broke down the 2026 OPPS Proposed Rule and called it a gold rush. The first tranche just hit: 285 procedures came off the inpatient-only list on January 1. The remaining 1,400+ will phase out by January 2028, and most of those will become ASC-eligible along the way.

But policy changes don’t move markets all on their own. Surgeons, facilities, and patients do. So we looked at what happened on the ground for a procedure that’s already been through this transition: total shoulder arthroplasty (CPT 23472).

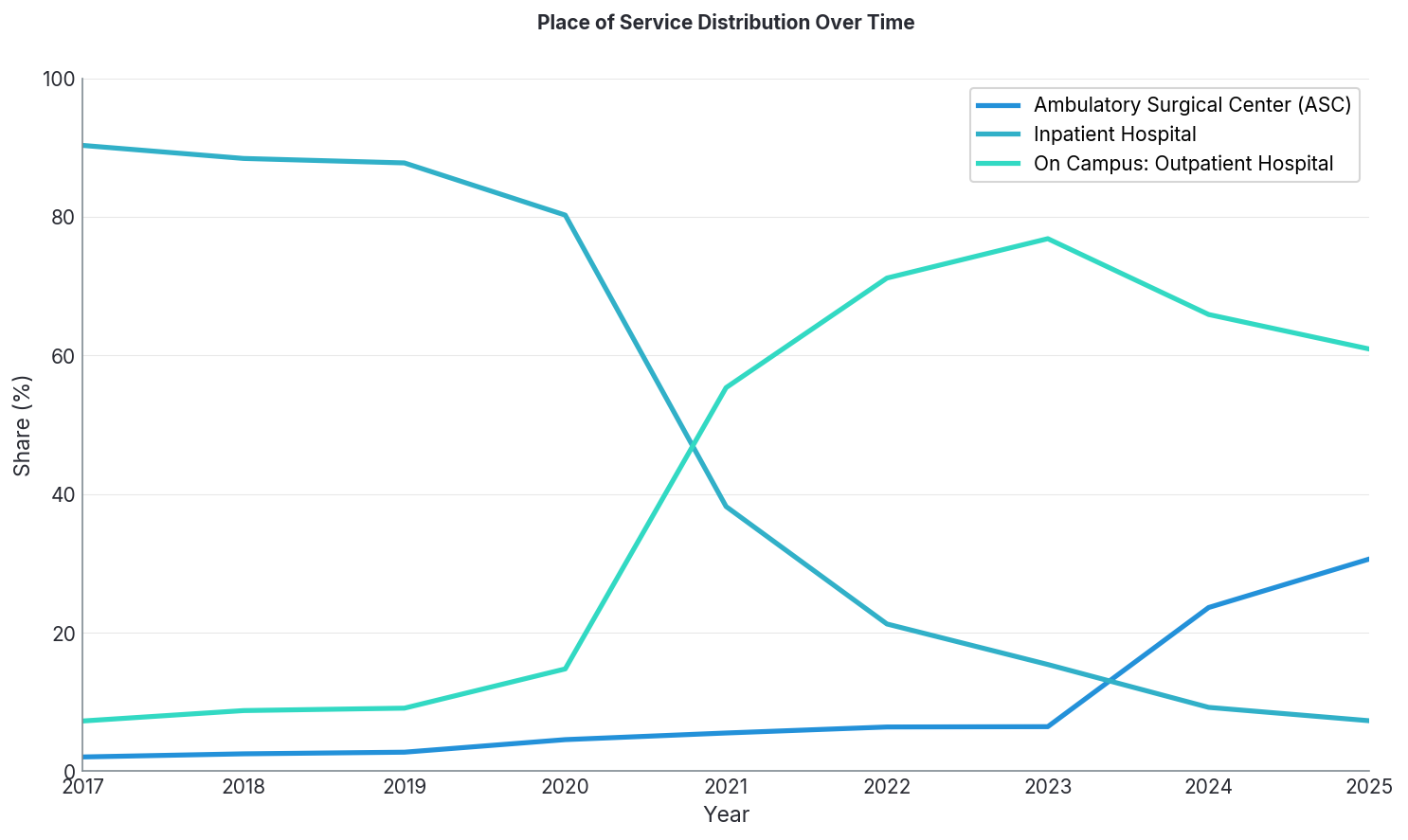

The short version: ASC share went from under 10% to over 30% in just two years.

What the national numbers say

Here’s what the place-of-service mix looks like for total shoulder arthroplasty:

Two inflection points worth noting.

When CMS removed it from the inpatient-only list in 2021, inpatient share cratered from 80% to 38% in a single year. The hospital outpatient absorbed most of that volume.

In 2024, when ASC eligibility kicked in, ASC market share nearly quadrupled, from 6.4% to 23.6%. Today, it’s over 30% and climbing.

Where the shift happens first

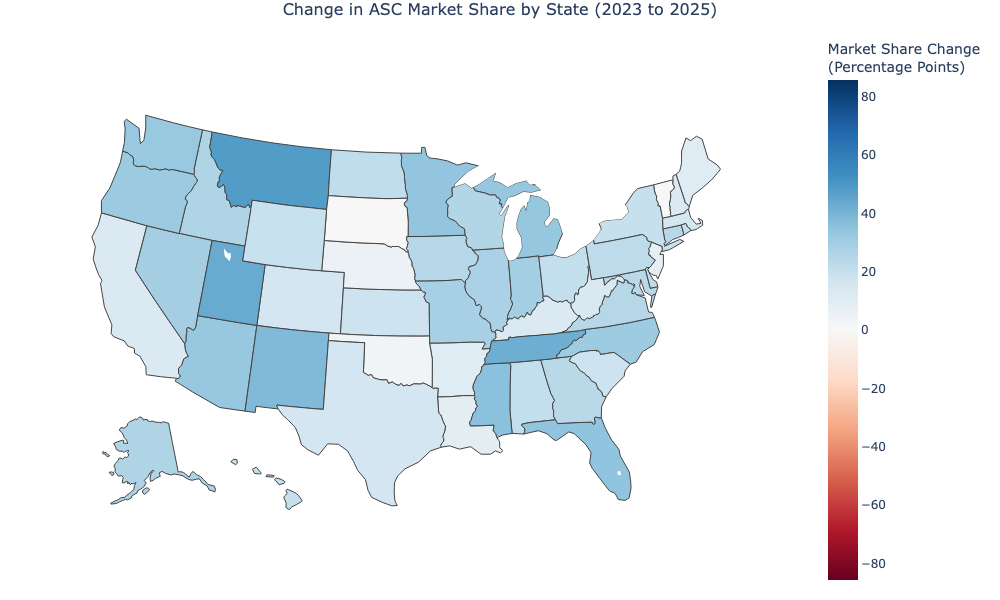

National averages tell part of the story, but early ASC adoption shows up unevenly across states.

We looked at state-level ASC volumes for shoulder arthroplasty in 2023 and again in 2025, right after ASC eligibility went into effect.

In terms of market share growth, Utah and Tennessee went from single-digit ASC market share to majority ASC, a fundamental rewiring of where care happens in those states. Montana led the way with a 48-point increase.

Here are the top 10 states in ASC market share growth:

| Rank | State | 2023 ASC Share | 2025 ASC Share | Percentage Increase |

| 1 | Montana | 10.5% | 58.6% | 48.1% |

| 2 | Utah | 8.5% | 52.0% | 43.5% |

| 3 | Tennessee | 8.9% | 51.0% | 42.1% |

| 4 | New Mexico | 17.6% | 55.5% | 37.9% |

| 5 | Mississippi | 18.1% | 53.9% | 35.8% |

| 6 | Florida | 4.6% | 39.1% | 34.5% |

| 7 | Minnesota | 6.9% | 40.8% | 33.9% |

| 8 | Michigan | 8.6% | 41.9% | 33.3% |

| 9 | Arizona | 9.5% | 42.3% | 32.8% |

| 10 | Washington | 12.5% | 44.9% | 32.4% |

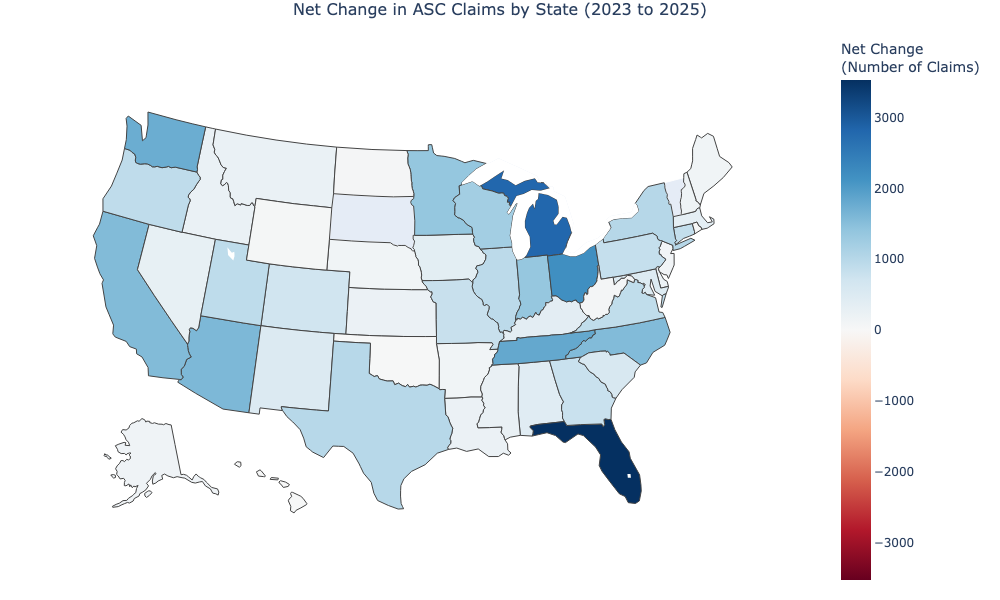

Now, in terms of absolute volume, Florida alone added 3,500+ shoulder replacement claims in the ASC setting in 2025 compared to 2023, and that’s without complete 2025 Medicare data from CMS (which we’ll be receiving soon).

Here are the top 10 states in claims growth:

| Rank | State | 2023 Claims | 2025 Claims | Net Change |

| 1 | Florida | 558 | 4,085 | 3,527 |

| 2 | Michigan | 826 | 3,631 | 2,805 |

| 3 | Ohio | 1,114 | 3,287 | 2,173 |

| 4 | Tennessee | 422 | 2,244 | 1,822 |

| 5 | Washington | 668 | 2,423 | 1,755 |

| 6 | Arizona | 492 | 2,092 | 1,600 |

| 7 | California | 763 | 2,318 | 1,555 |

| 8 | North Carolina | 256 | 1,808 | 1,552 |

| 9 | Minnesota | 360 | 1,735 | 1,375 |

| 10 | Indiana | 228 | 1,592 | 1,364 |

What this means for commercial strategy and territory design

There will be fast adopters.

Montana, Utah, Tennessee, New Mexico, and Mississippi all recorded over 35% growth in ASC market share. These may not be the highest-volume markets, but they move fast. If you have the headcount to expand into new territories before competitors do, these early-mover states can give you a head start.

There will be volume engines.

Other states drive opportunity through absolute volume. Florida, Michigan, and Ohio accounted for 8000+ more procedures done in ASCs in 2025 than in 2023. If this is an indicator of what will happen with other procedures, high-population, ASC regulation-friendly states like these represent the most significant near-term revenue opportunities.

There’s a sweet spot

The highest-leverage territories sit where we see both volume and growth. States like Tennessee, Michigan, and Florida are seeing rapid site-of-care migration alongside meaningful volume growth, making them strong candidates for a concentrated, ASC-focused strategy.

Ankle arthroplasty tells a similar story

We also looked into another procedure, total ankle arthroplasty (CPT 27702), which followed a similar CMS path: off IPO in 2021, ASC-payable in 2024.

For one, there are just way fewer ankle replacements than shoulder replacements, so we didn’t focus on it as much. And there has been a similar shift in place of service, but it’s been more gradual.

ASC share of ankle replacements:

4.1% in 2017 7.2% in 202120.1% in 2025Inpatient hospital dropped from 70.4% to 8.3% over that same period. Same directional story, just a different pace.

So what should device companies do with this?

Procedures moving off an inpatient-only list move the market considerably. Total shoulder arthroplasty shows how policy changes play out on the ground.

If your procedures became ASC-eligible (or will in the future), forecasting assumptions probably need to be revisited. Shoulder replacements went from 6% to 30%+ ASC share in two years. Some states are now at over 50% ASC. If territory plans and quota models assume gradual drift, you’re building on a faulty foundation. More to come on what we’re building to help.

A note on state-level data: Patterns can be affected by payer coverage and claims availability. Use these as strong directional signals, not 100% precise forecasts.

About Evan Knopp, Head of Market Strategy

Evan Knopp is the Head of Market Strategy at MedScout, where he leads positioning, competitive strategy, and market insight to drive growth. Prior to MedScout, he served as Head of Marketing at Turquoise Health and Director of Product Marketing at Sana Benefits, and held several marketing roles at IBM. Evan holds an MBA and a Bachelor’s degree from the University of Texas at Austin.

Bengali (Bangladesh) ·

Bengali (Bangladesh) ·  English (United States) ·

English (United States) ·